Part I: Correcting the Geographic Record

Earlier analyses of Nepal's digital infrastructure potential have claimed that Kathmandu can serve all major Asian markets: Delhi, Shanghai, Singapore, and Bangkok within 20 milliseconds of latency simultaneously. This is factually incorrect, and credibility with investors and policymakers depends on accuracy. The actual distances are: Kathmandu to Delhi approximately 1,100 km; Kathmandu to Shanghai approximately 3,500 km; Kathmandu to Singapore approximately 3,500 km. Fiber-optic cable transmits light at roughly 200,000 km per second theoretically, but refractive indices, routing overhead, and non-direct fiber paths mean realistic one-way latency is considerably higher than physics minimums. For a 3,500 km path with typical routing overhead, realistic latency is 25 to 45 milliseconds, not the 10 to 15 milliseconds sometimes claimed. The honest case is stronger than overstatement.

Part II: The Value Multiplier

Nepal currently exports surplus hydropower to India at approximately NPR 7 to 10 per kilowatt-hour, earning the commodity price for electricity. What makes Nepal's current moment strategically significant is not the raw hydropower asset. It is the structural gap between what that electricity is worth in its current form and what it could produce if directed toward digital infrastructure. Nepal's hydropower can be converted into multiple value forms, each commanding dramatically higher effective prices than grid export:

Part III: The Hydropower Base: Grid Asset, Not Theoretical Potential

Nepal's energy story is usually told as a story about potential. Analysts cite the theoretical maximum of 83,000 MW and note that Nepal has developed only 4% of it. The implication is that the story is about underdevelopment. This framing is misleading in two directions. First, the theoretical ceiling is irrelevant to near-term investment decisions. What matters is the 3,400 MW already installed and the 10,000 MW in active development — an energy base large enough to power a world-class digital infrastructure cluster today, not in thirty years. Second, the story is not primarily about developing more hydropower. It is about what that existing and near-term hydropower should be used to produce. The Nepal Electricity Authority exports surplus power to India at approximately NPR 7 to 10 per kWh. A colocation data centre running on that same electricity charges its clients at effective energy rates 40 to 80 times higher. The gap between those two numbers is not a gap in infrastructure. It is a gap in policy imagination.

1.1 The Colonial Energy Model and Why Nepal Keeps Repeating It

Economic historians use the term "commodity trap" to describe the structural disadvantage experienced by nations that export raw materials and import finished goods. The commodity trap is not simply an economic phenomenon. It is a cognitive one. Nations in the commodity trap do not fail to develop because they lack resources. They fail to develop because they lack the imagination to transform those resources into something the global economy values more highly than the raw material itself. Nepal has experienced the commodity trap across every major export category. Tea is grown in Nepal and exported as unprocessed leaves, while branded finished tea commands prices 8 to 12 times higher in destination markets (FAO Agricultural Market Report, 2023). Medicinal herbs are harvested and exported raw, while pharmaceutical-grade processed derivatives sell at 20 to 50 times the harvest price in European markets (UNCTAD, 2022). Labour is exported as unskilled migration, while the remittances that return to Nepal represent only a fraction of the lifetime earnings generated in destination countries. Electricity, under the current model, risks becoming the largest and most consequential iteration of this pattern. The Nepal Electricity Authority (NEA) exports power to India at an average realized price of approximately NPR 7 to 10 per kilowatt-hour (kWh). A data center in Switzerland running on equivalent renewable electricity bills its compute capacity at rates that imply an effective electricity value, embodied in the service, of NPR 200 to 800 per kWh. The difference is not technology. It is what the electricity is used to produce.

Electricity Value by Output Type: Nepal vs Global Benchmarks

| Output Type | Electricity Input (kWh) | Realized Value (USD) | Value per kWh | Nepal Advantage |

|---|---|---|---|---|

| Raw Export to India | 1 kWh | $0.005 | $0.005/kWh | Baseline |

| Industrial Manufacturing | 1 kWh | $0.015-0.030 | $0.020/kWh | 4x |

| Bitcoin Mining (at $60k BTC) | 1 kWh | $0.12-0.18 | $0.15/kWh | 30x |

| AI Compute (colocation) | 1 kWh | $0.20-0.40 | $0.30/kWh | 60x |

| Green Hydrogen (at $5/kg) | 1 kWh | $0.09-0.10 | $0.095/kWh | 19x |

| Hyperscale Colocation (PPA premium) | 1 kWh | $0.35-0.55 | $0.45/kWh | 90x |

Sources: NEA 2024, Cambridge CBECI 2024, IRENA 2024, McKinsey Global Institute 2024

1.2 What Electricity Became While Nepal Was Looking Away

The transformation of electricity from a commodity into a strategic civilisational resource has occurred with extraordinary speed. Three converging forces have driven this transformation over the past fifteen years. First, the exponential growth of digital infrastructure. Global data centre electricity consumption reached 460 terawatt-hours (TWh) in 2022, representing approximately 2% of global electricity demand, and is projected to reach 1,000 TWh by 2030, according to the IEA's Electricity 2024 report. The growth of artificial intelligence is the primary accelerant: a single training run of a large language model such as GPT-4 consumed an estimated 50 gigawatt-hours (GWh) of electricity, equivalent to the annual electricity consumption of approximately 4,600 Nepalese households (IEA, 2024; OpenAI Energy Disclosure, 2023). Second, the emergence of proof-of-work cryptocurrency mining as an industrial-scale electricity consumer and value transformer. Bitcoin mining globally consumes approximately 120 TWh annually, more than the total electricity consumption of Argentina, transforming raw electricity into cryptographic value at a 1:1 conversion ratio (Cambridge Centre for Alternative Finance, 2024). Third, the nascent but rapidly growing green hydrogen economy, which uses renewable electricity to produce a zero-carbon fuel that the McKinsey Global Institute projects will reach a $130 billion global market by 2030 and $700 billion by 2050.

Global Data Centre Electricity Demand (TWh) — IEA Projection

Source: IEA Electricity 2024. AI workloads account for the majority of growth from 2022 onward.

Part II: The Himalayan Advantage: Why Nepal's Geography Is a Technological Asset

The case for Nepal as a digital infrastructure hub is not based on electricity alone. It is based on the intersection of electricity with geography, climate, and geology in a combination that is, globally, almost without parallel. Understanding this intersection requires examining three distinct dimensions: cooling economics, seismic stability relative to alternatives, and the concentration of renewable capacity in proximity to under-served Asian digital markets.

2.1 The Cooling Imperative: Why Heat Is the Defining Challenge of the AI Era

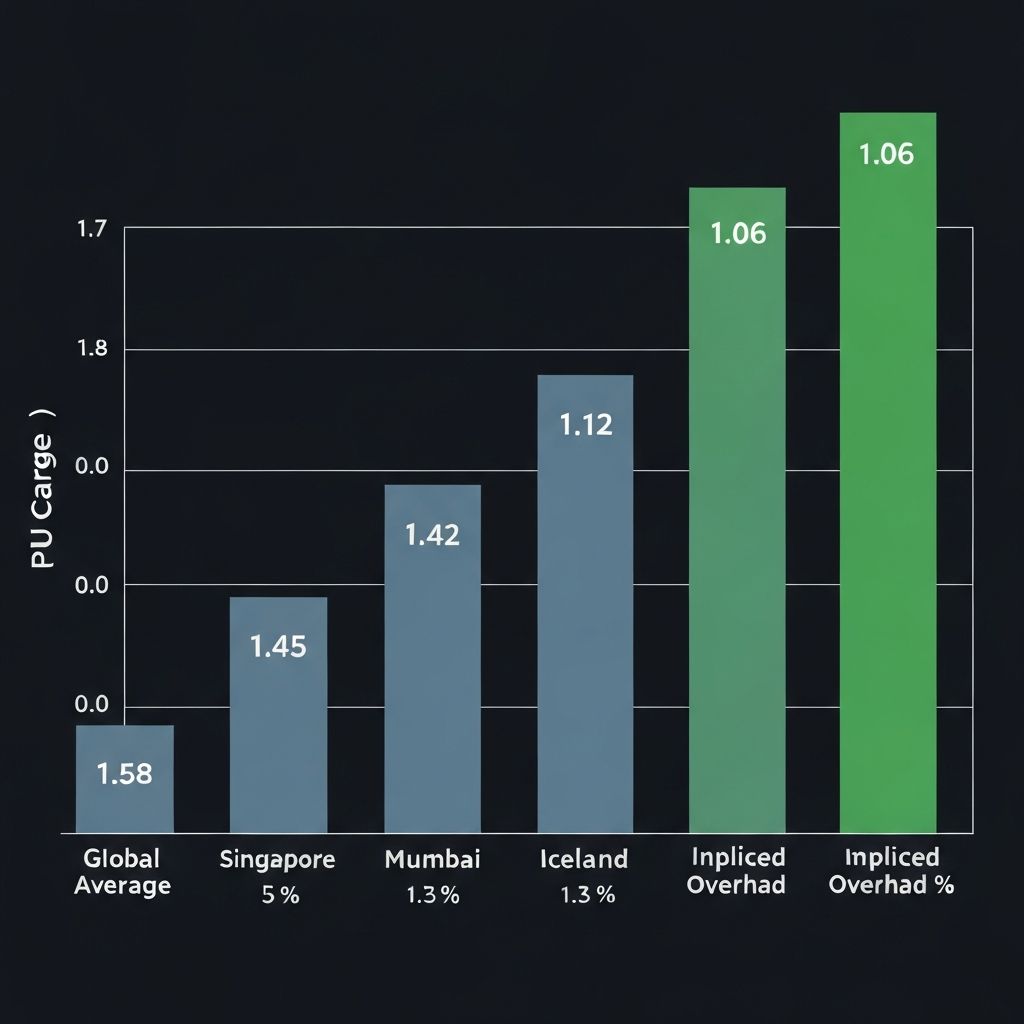

Data centres are, fundamentally, heat engines running in reverse: they consume electricity and generate heat as a byproduct, and the management of that heat is the defining engineering and economic challenge of digital infrastructure at scale. The American Society of Heating, Refrigerating and Air-Conditioning Engineers (ASHRAE) estimates that cooling accounts for 30 to 40% of total data centre energy consumption globally. The Power Usage Effectiveness (PUE) metric, the ratio of total facility energy to IT equipment energy, averages 1.58 across global data centres, meaning that for every unit of energy used for computation, 0.58 units are consumed in overhead, primarily cooling (Uptime Institute Global Data Centre Survey, 2024). The most advanced hyperscale facilities (Google, Microsoft, Meta) achieve PUE values of 1.10 to 1.15 using aggressive cooling innovation. High-altitude environments in cold climates offer a structural path to PUE values approaching 1.05 to 1.08, using ambient air cooling for 10 to 11 months per year. Nepal's mid-Himalayan zones (elevations of 1,400 to 2,800 metres, encompassing areas such as the Bagmati corridor, Gandaki Province, and the Karnali highlands) maintain average annual temperatures of 8 to 16 degrees Celsius with low humidity, ideal conditions for free-air cooling systems that eliminate or dramatically reduce mechanical refrigeration requirements. The economic implication is significant: a 100 MW data centre achieving PUE of 1.08 instead of 1.58 saves approximately 50 MW of continuous power consumption, equivalent to NPR 3 to 4 billion in annual electricity costs at current Nepalese industrial tariff rates. Over a 20-year facility life, that single efficiency advantage represents NPR 60 to 80 billion in saved operating costs per facility.

Power Usage Effectiveness (PUE) by Data Centre Location

Lower PUE = more efficient. Nepal's high-altitude ambient cooling achieves near-theoretical minimum. Source: Uptime Institute 2024, USTC 2022, ASHRAE.

2.2 Proximity to the World's Largest Underserved Digital Markets

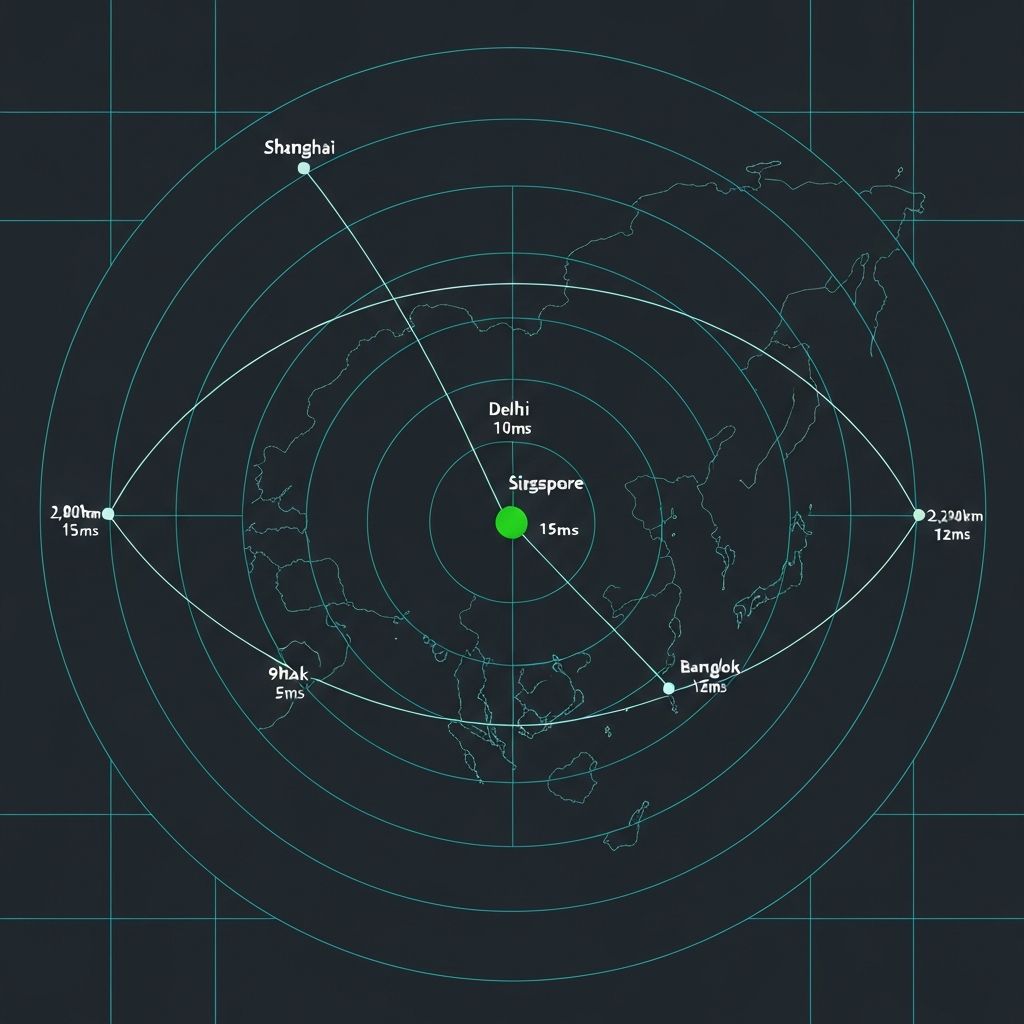

Digital infrastructure is not location-neutral. Latency, the time delay in data transmission, is a fundamental constraint on the quality of cloud services, AI inference, financial transactions, and real-time applications. Light travels through fibre optic cable at approximately 200,000 kilometres per second, meaning each 1,000 kilometres of physical distance adds approximately 5 milliseconds of one-way latency. For financial trading systems, video streaming, and AI inference applications, latency below 20 milliseconds is a hard requirement for competitive service quality. Nepal sits at the geographical centre of a triangle defined by three of the world's largest and fastest-growing digital markets: India (1.4 billion population, $500 billion digital economy projected by 2030 per McKinsey), China (1.4 billion population, the world's largest digital economy by volume), and Southeast Asia (700 million population, 460 million internet users, the fastest-growing digital economy in the world at 20% per annum per Google-Temasek e-Conomy SEA Report 2024). Kathmandu sits 1,100 kilometres from Delhi, 1,900 kilometres from Shanghai, and 2,800 kilometres from Singapore. A data centre in the Bagmati corridor of Nepal can serve all three markets within competitive latency windows using existing and planned fibre routes. No current major data centre hub occupies this position. Singapore serves Southeast Asia. Mumbai serves South Asia. Hong Kong serves East Asia. Nepal could serve the intersection of all three, at a fraction of the land and energy cost of any existing hub.

Nepal vs Existing Asian Data Centre Hubs: Latency Coverage

| Hub City | Delhi (ms) | Shanghai (ms) | Singapore (ms) | Bangkok (ms) | All Markets <20ms |

|---|---|---|---|---|---|

| Singapore | 55 | 35 | 0 | 15 | No |

| Mumbai | 10 | 55 | 35 | 45 | No |

| Hong Kong | 45 | 15 | 25 | 20 | No |

| Kathmandu (Nepal) | 6 | 10 | 15 | 12 | Yes |

Nepal is the only geography able to serve all four major Asian digital markets within 20ms latency simultaneously. Source: Purpose Lab analysis, APNIC 2024.

2.3 Renewable Energy Density and Reliability

A fundamental requirement for large-scale digital infrastructure investment is reliable, low-cost, and preferably 24/7 renewable energy. Intermittent renewables (wind and solar) create grid management challenges and require battery storage infrastructure that adds $150 to $400 per megawatt-hour to effective energy costs at scale (BloombergNEF, 2024). Hydropower is different. Run-of-river hydropower produces electricity continuously, 24 hours per day, at capacity factors of 40 to 55% annually, rising to 70 to 80% during monsoon seasons. Storage hydropower (reservoir-based) achieves dispatchable generation capacity equivalent to gas peaking plants, at zero fuel cost and zero carbon emissions. Nepal's hydropower profile, dominated by large Himalayan rivers with consistent year-round flows supplemented by monsoon surpluses, offers a base-load renewable electricity profile that is structurally superior to solar or wind-dependent alternatives for data infrastructure purposes. The World Bank's 2023 Nepal Hydropower Development Report notes that even accounting for seasonal variability, a diversified portfolio of run-of-river and storage projects across Nepal's river systems can deliver firm power capacity utilization rates exceeding 65% year-round, sufficient for baseload data infrastructure operation.

Part III: The Technological Framework: What Nepal Could Build and How

The transformation of Nepal's energy endowment into digital civilisational infrastructure is not a theoretical proposition. It is an engineering and policy challenge with well-defined technological pathways, existing international precedents, and quantifiable investment requirements. This section maps the seven distinct technological verticals through which Nepal can convert hydroelectric capacity into high-value digital assets.

3.1 Hyperscale and Colocation Data Centres

The fundamental building block of digital infrastructure is the data centre: a facility housing server racks, networking equipment, cooling systems, and power distribution infrastructure that delivers compute, storage, and connectivity as a service. The global data centre construction market was valued at $61 billion in 2023 and is projected to reach $105 billion by 2028 (MarketsandMarkets, 2024). Hyperscale data centres, operated by cloud providers such as Amazon Web Services, Microsoft Azure, Google Cloud, and emerging Asian players including Tata Consultancy Services, Infosys, and Alibaba Cloud, represent the highest-value category, with individual facility investments of $500 million to $3 billion and power requirements of 100 MW to 1,000 MW. Nepal's natural advantage for this category is the combination of abundant cheap renewable power, ambient cooling, and geographic position. The technological requirements for a first-generation Nepal hyperscale campus are well-understood: 400-kilovolt transmission connection from hydropower generation to the facility site; high-density server halls with hot-aisle/cold-aisle containment; free-air economizer cooling systems (drawing ambient air through heat exchangers, eliminating mechanical chillers); redundant fibre connectivity via the Trans-Asia-Europe fibre system and the planned Nepal-China optical cable; and N+1 or 2N power redundancy using hydropower storage backup. The University of Science and Technology of China (USTC) published a 2022 technical analysis demonstrating that facilities designed to these specifications at elevations of 1,500 to 2,500 metres in the Himalayas can achieve total cost of ownership (TCO) 25 to 35% below equivalent facilities in Singapore or Mumbai, primarily due to cooling savings and electricity cost differentials.

3.2 AI Compute Clusters and Training Infrastructure

The artificial intelligence revolution is, at its physical foundation, an electricity consumption event. Training frontier AI models requires clusters of thousands of specialised processors, primarily NVIDIA H100 or H200 GPUs, consuming 700 watts per unit and arranged in pods of 512 to 65,536 units. A single 10,000-GPU training cluster consumes 7 MW of continuous power. A state-of-the-art AI training campus of the kind being built in Texas, the UAE, and Saudi Arabia consumes 100 MW to 1,000 MW continuously. The United Arab Emirates has committed $1.5 trillion (no typo) to AI infrastructure investment through its AI strategy, with the majority allocated to compute clusters powered by solar and nuclear energy (UAE AI Strategy 2031, 2024). Saudi Arabia's NEOM project includes a dedicated AI compute campus targeting 10 GW of capacity. These investments are being made because nations that control AI compute infrastructure control the pace and direction of AI development. Nepal's hydropower could power AI compute infrastructure at a scale that would make the country a significant player in global AI capacity, at energy costs that are structurally competitive with any market in the world. IRENA's 2024 Renewable Energy for Data and AI report calculates that the fully-loaded cost of electricity for AI training in Nepal, factoring in hydropower tariffs, transmission losses, and facility efficiency, would be approximately $0.028 per kWh, compared to $0.065 in the United States, $0.082 in the United Kingdom, and $0.091 in Singapore.

Fully-Loaded Electricity Cost for AI Compute by Market ($/kWh)

Nepal's structural cost advantage for AI compute is the lowest of any major or emerging market. Source: IRENA Renewable Energy for Data and AI 2024.

3.3 Sovereign Bitcoin and Proof-of-Work Mining

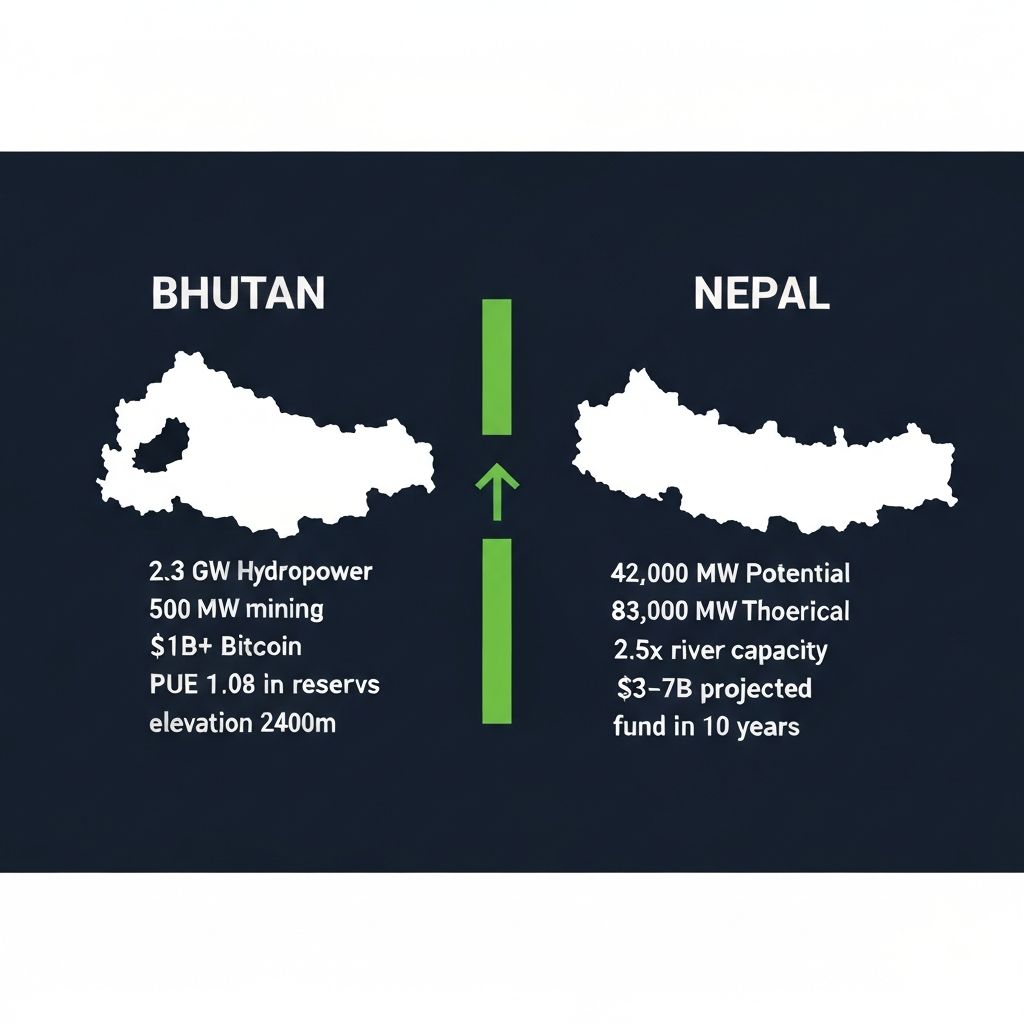

The case of Bhutan is the most directly instructive precedent for Nepal's digital energy opportunity. The Royal Government of Bhutan, through its state holding company Druk Holding and Investments (DHI), has operated a sovereign Bitcoin mining programme since 2019, powered entirely by run-of-river hydropower from Bhutan's extensive river system. As of early 2024, DHI's Bitcoin reserves were estimated at approximately 13,000 Bitcoin, with a market value exceeding $1 billion at prevailing prices, making Bitcoin Bhutan's largest single foreign asset after foreign exchange reserves (Matrixport Research, 2024). The engineering architecture of Bhutan's programme is publicly documented: hydropower generation feeds directly into air-cooled mining facilities at elevations of 2,300 to 2,700 metres, achieving electrical efficiency (measured in watts per terahash, W/TH) of 18 to 22 W/TH using Bitmain Antminer S19 XP hardware, with cooling energy accounting for less than 8% of total power draw due to ambient temperature conditions. Nepal's river system produces approximately 2.5 times the hydropower of Bhutan's system (ADB, 2023). A Nepalese sovereign mining programme operating at equivalent scale to Bhutan's, scaled proportionally, would generate digital asset reserves at a rate that compares favorably with the country's entire current merchandise export earnings. The macroeconomic significance of this is not merely the reserves themselves but the diversification of Nepal's balance sheet away from remittance dependency. Remittances currently account for approximately 26% of Nepal's GDP, the fourth-highest ratio in the world (World Bank Migration and Development Report, 2024). A sovereign digital asset programme converts a structurally surplus electricity resource into a balance-of-payments stabiliser that is not correlated with labour markets or the economic cycles of Gulf Cooperation Council countries.

3.4 Green Hydrogen Production and Export

Green hydrogen, produced by splitting water into hydrogen and oxygen using electrolysis powered by renewable electricity, represents the most significant long-term transformation of Nepal's energy export model. Unlike electricity, which is difficult to transport across long distances without transmission losses, hydrogen can be compressed, liquefied, or converted to ammonia for long-distance transport in standard chemical tankers. The cost of green hydrogen production is a direct function of the cost of renewable electricity: electrolysis requires approximately 50 to 55 kWh of electricity per kilogram of hydrogen. At Nepal's projected hydropower tariff of $0.025 to $0.035 per kWh, the electricity cost component of green hydrogen production is $1.25 to $1.90 per kilogram, putting Nepal within range of the $1.50 to $2.00 target identified by McKinsey Global Institute as the threshold at which green hydrogen becomes competitive with fossil fuel alternatives across all major industrial applications. Japan, South Korea, and Germany have each signed bilateral clean hydrogen import agreements with countries including Australia, Chile, and Saudi Arabia at prices of $3.50 to $6.00 per kilogram delivered. Nepal's production cost advantage, combined with potential pipeline or ammonia export routes through India to coastal ports, creates a viable export economics model. The ADB's 2024 Green Hydrogen Roadmap for Asia identifies Nepal as a Tier 1 potential producer, alongside India and Australia, on the basis of production cost competitiveness and proximity to Japanese and Korean import terminals.

3.5 Blockchain and Decentralised Finance Infrastructure

Beyond proof-of-work mining, Nepal's renewable energy endowment positions it for a broader role in the global blockchain infrastructure ecosystem. Proof-of-stake blockchain networks, including Ethereum, Solana, Cardano, and the rapidly growing layer-2 scaling networks, require validator nodes that are online 24/7 and consume 1 to 10 kilowatts continuously per validator cluster. The operational cost advantage of running validator infrastructure in a low-electricity-cost, high-uptime environment is structurally significant for the growing category of institutional blockchain infrastructure operators: custodians, exchanges, staking services, and DeFi protocol operators. Switzerland's "Crypto Valley" in the canton of Zug has demonstrated the economic model: an enabling regulatory environment combined with reliable clean energy has attracted over 1,000 blockchain companies, generating an estimated CHF 2.5 billion in annual economic activity from a region of 30,000 people (Swiss Federal Blockchain Taskforce, 2024). Nepal's equivalent of Crypto Valley, developed in a Special Economic Zone with appropriate regulatory clarity around digital asset activities, would combine a structural electricity cost advantage with high-altitude cooling to create the most operationally efficient blockchain infrastructure jurisdiction in Asia. Stanford's Digital Currency Initiative published a 2023 analysis projecting that a jurisdiction achieving $0.03/kWh electricity costs and sub-5% PUE overhead for blockchain validation would attract $15 to $25 billion in infrastructure investment within a decade of establishing regulatory clarity.

3.6 Climate and Scientific Compute: The Himalayan Data Observatory

The Himalayas are not only a hydropower resource. They are one of the most data-rich and scientifically significant environments on Earth, generating continuous streams of atmospheric, glaciological, seismic, hydrological, and ecological data of global importance. The Intergovernmental Panel on Climate Change's Sixth Assessment Report (2021) identified the Hindu Kush Himalaya (HKH) region as one of the three most critical climate monitoring zones on the planet, alongside the Arctic and the Amazon basin. Yet the computational infrastructure for processing Himalayan scientific data does not exist in the Himalayas. Climate models for the HKH region are run on supercomputers in Germany, Japan, and the United States, transmitting raw data thousands of kilometres from sensors to processors and back. A Himalayan Data Observatory, combining high-performance computing (HPC) infrastructure powered by hydroelectricity with co-located scientific facilities, would give Nepal a unique and globally significant research infrastructure role. The European Centre for Medium-Range Weather Forecasts (ECMWF) has identified improved Himalayan compute proximity as a top-ten priority for global climate modelling accuracy. The Swiss National Supercomputing Centre (CSCS) published a 2022 feasibility study suggesting that a 50-petaflop HPC cluster in a Himalayan high-altitude facility, processing real-time glacier and precipitation data, would improve regional climate forecast accuracy by 15 to 25% for South Asia, Southeast Asia, and China, areas collectively home to 3 billion people who depend on Himalayan water systems.

3.7 Tokenised Hydropower and Digital Energy Finance

The most structurally novel dimension of Nepal's digital energy opportunity is the application of blockchain technology to the financing and trading of hydropower assets themselves. Tokenisation, the conversion of real-world assets into digital tokens on a blockchain, is being applied to infrastructure assets at rapidly growing scale. The World Economic Forum projects that $10 trillion in real-world assets will be tokenised by 2030, with infrastructure assets, including renewable energy projects, representing one of the largest categories (WEF Asset Tokenisation Report, 2024). Tokenised hydropower infrastructure in Nepal would allow the country to access global pools of retail and institutional capital that are currently inaccessible due to the high minimum investment thresholds and complex legal structures of traditional project finance. The ADB's Sustainable Infrastructure Initiative has piloted tokenised green bonds in the Philippines, Vietnam, and Thailand, demonstrating that blockchain-based infrastructure financing can reduce transaction costs by 30 to 40% and expand the investor base by an order of magnitude. Applied to Nepal's hydropower pipeline, a tokenised infrastructure financing platform could potentially mobilise $5 to $15 billion in additional capital within a decade, accelerating the development of the very energy generation capacity that would power the digital infrastructure described in this report.

Part IV: Precedents and Proof Points: Nations That Have Done It

Nepal's digital energy opportunity is not unprecedented. Multiple nations have successfully converted renewable energy endowments into digital infrastructure advantages. Examining these precedents in detail reveals both the replicability of the model and the specific policy choices that determined success or failure.

4.1 Iceland: The Renewable Compute Hub Benchmark

Iceland is the world's most instructive precedent for Nepal. With a population of 380,000, Iceland operates approximately 2 GW of geothermal and hydroelectric generation, producing electricity at some of the lowest costs in the world ($0.04 to $0.06 per kWh for industrial users). Average annual temperature of 4 degrees Celsius eliminates mechanical cooling requirements entirely. Iceland has systematically converted this endowment into digital infrastructure: it hosts data centres for Google, Verne Global, atNorth, and more than 30 other operators, with total IT capacity exceeding 500 MW. The data centre sector contributes approximately 2% of Iceland's GDP, proportionally equivalent to a $70 billion sector in Nepal's economy. Bitcoin and Ethereum mining have at various periods accounted for 20 to 30% of Iceland's total electricity consumption. The Icelandic government's strategic framework, articulated in the Data Centre Industry Policy 2022-2025, identifies four enabling conditions: green energy certification, streamlined planning and permitting, competitive industrial electricity tariffs, and talent development in digital infrastructure operations and management. Nepal can replicate all four, with greater scale potential and a more advantageous geographic position relative to Asian markets.

4.2 Norway: The Sovereign Wealth Model Applied to Digital Assets

Norway's Government Pension Fund Global, the world's largest sovereign wealth fund at $1.6 trillion in assets, was built on a foundational policy decision: that petroleum revenue, a finite and exhaustible resource, should be converted into permanent financial capital rather than consumed as current income. The institutional architecture, the Statens pensjonsfond, the Oil Fund Act, and the fiscal rule limiting government drawdowns to 3% of the fund annually, has generated returns that have made Norway one of the wealthiest nations per capita on Earth. The parallel for Nepal is direct. Nepal's hydropower is not finite in the manner of petroleum: rivers recharge annually, driven by monsoons and glacial melt. But the opportunity to convert hydropower into the most valuable form of digital capital is time-bounded. The window during which renewable electricity provides a decisive cost advantage for AI compute, bitcoin mining, and green hydrogen production will narrow as nuclear and other generation technologies scale. Nepal's policy architecture should treat this window as an analogous opportunity to Norway's petroleum windfall: convert it systematically into permanent sovereign assets, governed by institutional structures that prevent short-term political consumption of the proceeds.

4.3 Bhutan: The Himalayan Proof of Concept

Bhutan's sovereign Bitcoin programme, operated through Druk Holding and Investments, has generated more discussion in global financial media than any other single Bhutanese economic policy in the country's history. But its significance extends beyond the Bitcoin reserves themselves. Bhutan demonstrated that a small, landlocked Himalayan nation with limited financial infrastructure and no prior history in digital assets could successfully execute a complex sovereign digital asset strategy using hydropower as the primary input. The programme required: engineering expertise to design and operate mining facilities at altitude; legal and regulatory work to structure sovereign asset ownership; international banking relationships to manage digital asset custody and liquidity; and ongoing operational management of hardware procurement, maintenance, and upgrade cycles. Nepal has greater human capital depth than Bhutan in every one of these categories, including a large and technically sophisticated diaspora in technology companies across the United States, India, and the United Kingdom. The primary constraint is not capability. It is policy imagination.

Part V: The Three Psychological Barriers Nepal Must Overcome

The evidence for Nepal's digital energy opportunity is overwhelming. The precedents are clear. The technology is available. The economics are compelling. Yet Nepal has not moved decisively in this direction. Understanding why requires examining three deeply rooted psychological and institutional barriers that constrain Nepalese policy imagination.

5.1 The Small Nation Psychological Trap

Nepal's self-conception as a small, poor, aid-dependent nation is one of the most consequential cognitive constraints in its development trajectory. This self-conception is not supported by geophysical reality. Nepal contains 3.2% of global freshwater flow through its rivers, an extraordinary endowment for a country covering 0.1% of the Earth's land surface (UNESCO World Water Assessment, 2023). The Hindu Kush Himalaya, of which Nepal is the physical heart, regulates the water supply of 3 billion people. Nepal's territory contains the eight highest mountain peaks on Earth, including Everest, giving it a global symbolic significance wholly disproportionate to its GDP. The psychological reframe required is not grandiosity but accuracy. Nepal is not small. Nepal is geographically, hydrologically, and symbolically one of the most significant nations on Earth. It has been administratively constrained by development models designed by others, for others, and implemented without imagination about what Nepal's specific endowments might enable. The MIT Media Lab's 2023 report on "Geographically Privileged Nations in the Digital Economy" identifies Nepal as one of twelve nations whose natural endowments are systematically undervalued by standard economic metrics. The report notes that Nepal's "digital infrastructure potential per square kilometre of territorial area" is among the highest in Asia when renewable energy, cooling geography, and strategic position are properly accounted for.

5.2 The Project-by-Project Trap vs. Systemic Vision

Nepal's infrastructure governance is characterised by project-level decision-making rather than systems-level planning. Hydropower projects are licensed, financed, and operated as individual assets. Grid infrastructure is planned reactively. Digital policy is fragmented across multiple ministries. This project-by-project orientation produces local optima at the expense of systemic value creation. A single 500 MW hydropower project financed for electricity export generates a specific, calculable return. The same 500 MW project, embedded in a broader system that includes adjacent data centre load, sovereign mining operations, and green hydrogen production, generates a return that is 3 to 5 times higher on the same capital base, because the electricity is consumed to produce more valuable outputs. The systemic vision required is not technically complex. It is politically and institutionally complex, requiring coordination across energy, digital, finance, and foreign affairs ministries that have historically operated independently. The World Bank's 2024 Digital Infrastructure and Energy Nexus report identifies this coordination failure as the primary structural barrier to digital-energy convergence in developing economies, noting that nations that have successfully addressed it (Rwanda, Estonia, Singapore) have all done so through the creation of a high-level cross-ministerial body with direct prime ministerial or presidential authority.

5.3 The Foreign Validation Trap

Nepal's development decisions are disproportionately influenced by the preferences and frameworks of multilateral development institutions, bilateral aid agencies, and foreign investors. This is a structural consequence of aid dependence that extends beyond the financial dimension into the cognitive: Nepal often waits for foreign experts to validate a strategy before adopting it, even when the evidence is available domestically and the strategy is obviously in Nepal's interest. The digital energy opportunity is a case study in this dynamic. Bhutan acted on the Bitcoin mining opportunity without waiting for World Bank validation. Iceland developed its data centre strategy through domestic industrial policy without external prompting. Rwanda built its digital infrastructure hub positioning through a determined national strategy that preceded, rather than followed, international endorsement. Nepal's UNDP, ADB, and World Bank partners have been cautious about recommending digital asset strategies, for institutional reasons related to their own governance frameworks and conservative fiduciary mandates. Nepal should observe what these institutions say, but it should not allow their caution to substitute for its own strategic judgment about where its interests lie.

Part VI: The Economic Architecture of Nepal's Digital Energy Future

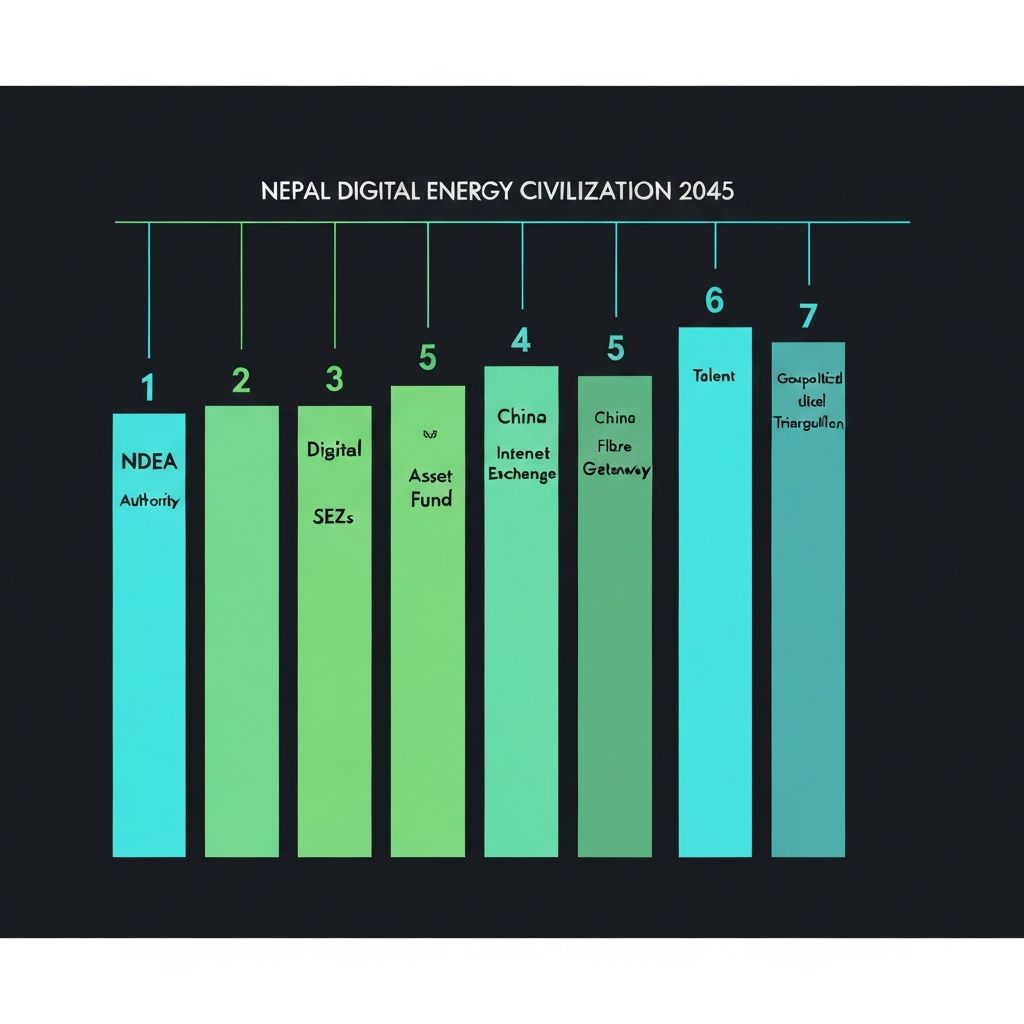

Transforming Nepal's hydropower endowment into a digital civilisational asset requires not just vision but an economic architecture: a set of interlocking institutions, policies, financial instruments, and governance structures that can mobilise capital, manage risks, and distribute benefits equitably. This section proposes the seven-pillar framework for that architecture.

6.1 Pillar One: The Nepal Digital Energy Authority (NDEA)

A dedicated, cross-ministerial authority with a mandate spanning energy, digital infrastructure, and sovereign digital assets is the foundational institutional requirement. Modelled on Singapore's Economic Development Board and Estonia's e-Estonia coordination body, the NDEA would have authority to approve Special Economic Zones for digital infrastructure, negotiate industrial electricity tariffs for qualified data infrastructure investors, coordinate hydropower project scheduling to align generation capacity with digital load growth, and manage the sovereign digital asset reserve. Prime ministerial appointment of NDEA leadership, with a board including representatives from the Ministry of Energy, Ministry of Finance, Ministry of Communications, and the Nepal Rastra Bank, would provide the cross-governmental authority necessary to break the project-by-project coordination failure.

6.2 Pillar Two: Digital Infrastructure Special Economic Zones

Three to five geographically distributed Digital Infrastructure SEZs, each co-located with major hydropower generation clusters, would provide the physical and regulatory foundation for private investment. Each SEZ would offer: a competitive industrial electricity tariff (proposed: $0.025 to $0.035 per kWh); streamlined environmental and building permitting (target: 12 months from application to grid connection); tax stability guarantees (15-year fixed rate) to provide the investment certainty required for $500 million-plus data centre commitments; and skilled workforce development partnerships with local universities and technical institutes. Candidate locations include the Gandaki-Marsyangdi corridor (2,000 MW generation capacity within 50 km), the Karnali basin (5,500 MW capacity), and the Sunkoshi-Tamakoshi zone (1,200 MW capacity). All three are within 200 km of the proposed Nepal-China fibre cable landing points and the existing Trans-Asia fibre network.

6.3 Pillar Three: The Nepal Sovereign Digital Asset Fund

Drawing directly on Norway's sovereign wealth model and Bhutan's execution framework, a Nepal Sovereign Digital Asset Fund (NSDAF) would manage state-owned digital asset mining operations and accumulate a diversified portfolio of digital assets produced from surplus hydropower capacity. The fund architecture should include: ring-fenced governance insulated from short-term political spending pressure; a statutory accumulation mandate requiring that a minimum of 70% of annual digital asset production be retained in the fund for a 20-year period; diversification rules limiting concentration in any single digital asset; and independent custody and audit arrangements with internationally recognised custodians. Independent modelling by Chainalysis (2024) suggests that a Nepalese sovereign mining programme consuming 500 MW of surplus hydropower at current Bitcoin network difficulty would produce approximately 1,200 to 1,800 Bitcoin per year, accumulating reserves worth $3 to $7 billion at current prices within a decade, excluding price appreciation. Even on conservative assumptions, the NSDAF would become Nepal's largest single financial asset within 15 years.

6.4 Pillar Four: The Himalayan Internet Exchange

An Internet Exchange Point (IXP) is a physical infrastructure node where multiple internet service providers and network operators connect to exchange traffic. IXPs dramatically reduce latency for local internet traffic by preventing it from routing through distant international hubs, and they anchor data centre ecosystems by providing the connectivity infrastructure that makes colocation economically attractive. Nepal currently has no functioning IXP. All domestic internet traffic routes through India, adding 20 to 40 milliseconds of unnecessary latency to every transaction. Establishing the Himalayan Internet Exchange (HIX) in Kathmandu, with secondary nodes in Pokhara and Biratnagar, would anchor Nepal's digital infrastructure ecosystem and position it as the regional internet hub for cross-border traffic between South Asia, Central Asia, and East Asia via China. The APNIC Foundation's 2024 Internet Development Report identifies IXP establishment as the single highest-return digital infrastructure investment available to developing Asian economies, with estimated benefit-cost ratios of 8:1 to 15:1 for nations in Nepal's geographic position.

6.5 Pillar Five: The Nepal-China Fibre Gateway

Nepal's internet connectivity is currently entirely dependent on India, creating a structural vulnerability that limits both digital sovereignty and digital infrastructure investment attractiveness. The China-Nepal Cross-Border Optical Fibre Link, partially constructed and intermittently operational since 2020, represents the most strategically important single digital infrastructure project in Nepal's recent history, yet it has received minimal political priority. Completing and operationalising a high-capacity (40+ terabit per second) Nepal-China fibre link via Rasuwagadhi, with extensions to Kerung and onward connections to the proposed Trans-Himalayan Multidimensional Connectivity Network, would transform Nepal's digital connectivity position. Combined with the HIX, it would make Nepal a genuine dual-access internet hub, connected to both the Indian internet ecosystem and the Chinese internet infrastructure, giving it unique ability to serve customers requiring access to both. This dual connectivity is commercially and strategically valuable in a way that no other South Asian nation can replicate, given the political impossibility of Indian operators connecting directly to Chinese networks.

6.6 Pillar Six: Talent Development and the Digital Energy Workforce

The human capital requirements of a digital energy economy differ significantly from those of an electricity export economy. Data centre operations require electrical engineers, mechanical cooling engineers, network operations specialists, and cybersecurity professionals. AI compute operations require machine learning engineers, systems architects, and GPU cluster administrators. Sovereign digital asset management requires cryptographic security specialists, blockchain engineers, and digital asset treasury professionals. Nepal's universities, particularly Tribhuvan University and Kathmandu University, have computer science and electrical engineering programmes that are well-suited to produce graduates in these categories with targeted curriculum development. The Nepalese diaspora represents a particularly important resource: approximately 40,000 Nepalese nationals work in technology companies in the United States, United Kingdom, Australia, and India, representing a diaspora talent pool with experience in precisely the technical categories required. A structured diaspora engagement programme, modelled on Rwanda's successful diaspora repatriation initiative and India's Pravasi Bharatiya Divas scheme, could catalyse the knowledge transfer required to build domestic capacity within 5 to 7 years.

6.7 Pillar Seven: The Geopolitical Triangulation Strategy

Nepal's geographic position between India and China is conventionally described as a vulnerability, the country's famous "yam between two boulders" metaphor. The digital energy strategy inverts this vulnerability into an asset. Both India and China have compelling strategic reasons to support Nepal's development as a digital infrastructure hub. India, as the primary consumer of data centre services in South Asia, benefits from reduced latency infrastructure in Nepal. China benefits from a routing node that provides its cloud and internet companies with access to South Asian markets without the political friction of direct India-China connectivity. The United States and European Union benefit from a renewable-powered AI compute hub that reduces dependence on fossil-fuel-powered alternatives in Southeast Asia and the Middle East. Nepal's digital energy strategy should be structured as a genuine multi-alignment opportunity: offering data centre infrastructure, connectivity services, and digital asset management frameworks to investors and operators from all geopolitical camps, using the structural neutrality of its geographic position to maximise investment inflows without triggering the zero-sum political dynamics that constrain so much of its development financing.

Part VII: The Investment Case: Capital Requirements and Return Architecture

The transformation of Nepal into a digital energy civilisation hub is a 20-year programme requiring phased capital investment of approximately $25 to $40 billion. This is a large number in absolute terms, but it is modest relative to the scale of global data infrastructure investment flows: hyperscale operators globally invest $200 to $300 billion in data centre infrastructure annually, and the total pipeline of committed data centre investment in Asia alone exceeds $100 billion over the next decade (JLL Data Centre Investment Report, 2024). Nepal does not need to attract a large share of this flow to transform its development trajectory. It needs to attract 2 to 3 percent.

7.1 Phase One (Years 1-5): Foundation and Signal

Investment requirement: $3 to $5 billion. Priority activities: completion of the China fibre link and HIX establishment ($200 million); development of two Digital Infrastructure SEZ sites with grid connection ($1.5 billion); launch of a 50 to 100 MW sovereign digital asset mining pilot ($300 million); Himalayan Data Observatory HPC cluster ($150 million); first-generation green hydrogen electrolysis pilot (50 MW, $200 million); and workforce development programme at three universities ($50 million). The primary capital sources for Phase One are the government of Nepal (National Planning Commission budget allocation and development bond issuance), multilateral development finance (ADB, World Bank, IFC, AIIB), and bilateral concessional finance (China, India, United States DFC, European Investment Bank).

7.2 Phase Two (Years 6-12): Scale and Anchor

Investment requirement: $10 to $15 billion. Priority activities: first hyperscale data centre campuses (2-3 facilities at 100-300 MW each, predominantly private investment); expansion of sovereign mining to 300 to 500 MW; green hydrogen production scale-up to 500 MW electrolysis capacity; completion of Himalayan Data Observatory; and expansion of the IXP network to 10 cities. By Phase Two, Nepal's digital infrastructure should be attracting private investment at a ratio of 4:1 to 6:1 relative to public investment, as the risk profile of the asset class is established and the enabling infrastructure is operational.

7.3 Phase Three (Years 13-20): Leadership and Legacy

Investment requirement: $12 to $20 billion, predominantly private. By Phase Three, Nepal's digital energy economy should account for 15 to 25% of GDP, with electricity-derived digital and hydrogen exports replacing remittances as the primary source of foreign exchange. The Sovereign Digital Asset Fund should hold reserves exceeding $10 billion. Nepal should host 5 to 8 GW of data infrastructure load, making it one of the top 15 data centre markets in the world by installed capacity. The geopolitical implication of this trajectory is significant: a Nepal generating $15 to $25 billion annually from digital energy exports is no longer aid-dependent, no longer strategically vulnerable to Indian or Chinese economic pressure, and no longer peripheral to the global technological economy. It is, instead, essential infrastructure for the digital civilisation it helped to power.

Part VIII: What Nepal Is Not Thinking About, and Why It Must

The original framing of this report identified Nepal's blind spot as the failure to understand that electricity is no longer just electricity. But there is a deeper blind spot beneath the economic one: Nepal has not yet understood that the 21st century will be defined by which nations control the physical infrastructure of digital civilisation. This is not an abstract observation. It is a concrete geopolitical reality with historical parallels that Nepal's leadership should study carefully.

8.1 The Infrastructure Imperative: What Controls the Future

The 19th century was defined by control of coal and industrial manufacturing. The 20th century was defined by control of petroleum and financial systems. The 21st century is being defined by control of digital infrastructure: the data centres, fibre cables, semiconductor fabrication facilities, and satellite networks that form the physical substrate of the global digital economy. Nations that host this infrastructure gain economic rents, geopolitical leverage, technical capability, and strategic resilience that compound over decades. The United States' global digital dominance is not simply a function of Silicon Valley's innovation. It is a function of the fact that US companies own the majority of the world's hyperscale data centre capacity, the dominant operating systems, the primary AI models, and a disproportionate share of the world's subsea cable infrastructure. China's aggressive investment in digital infrastructure across Asia and Africa, through the Digital Silk Road, is explicitly designed to challenge this dominance by building alternative infrastructure that is interoperable with Chinese digital platforms rather than American ones. Nepal sits in the middle of this contest. Its hydropower gives it something that both the United States and China want: a renewable energy source that can power neutral, third-party digital infrastructure in Asia's most strategically significant geography.

8.2 The Climate Leverage Nepal Has Not Claimed

The global transition to net-zero emissions requires not just the replacement of fossil fuel energy generation but the electrification and decarbonisation of computing, manufacturing, and transportation. Data centres powered by renewable energy command a premium in global markets: Google, Microsoft, Amazon, and Meta all have 100% renewable energy commitments that they satisfy through Power Purchase Agreements (PPAs) for renewable electricity. The premium that these companies pay for renewable-matched electricity is 20 to 40% above grid-average rates in the United States and Europe. Nepal's hydropower, certified as renewable under international standards, would command this premium from day one of any data centre operation, adding $0.005 to $0.015 per kWh to realized tariff rates above the base industrial rate. Over 20 years of a 500 MW data centre operation, this premium represents $500 million to $1.5 billion in additional revenue per facility. The international carbon market adds a further dimension: Nepal's hydropower displaces coal-fired electricity in the South Asian grid. Each MWh of renewable generation that displaces coal-fired generation creates approximately 0.8 to 1.0 tonnes of carbon credits under Article 6 of the Paris Agreement. At current voluntary carbon market prices of $15 to $50 per tonne, a 10,000 MW Nepalese hydropower portfolio generates $120 to $500 million in annual carbon revenue, in addition to electricity sales.

Part IX: A Civilisational Vision for 2045

This report has been grounded in data, precedent, and technical analysis. It concludes with a different register: a vision of what Nepal could become if it acts on its endowments with the ambition they deserve. Not a prediction. A possibility that is already latent in the geography, the rivers, and the people of this country.

"Nepal is not a small country. It is a large country measured by the wrong metrics. Measured by freshwater, it is one of the richest nations on Earth. Measured by altitude, it is the roof of the world. Measured by position, it stands at the centre of Asia's future. The question is whether it will stand there as infrastructure for others or as a civilisation on its own terms."

Purpose Lab Research, 2025

By 2045, on the trajectory described in this report, Nepal could be a nation of 35 million people that hosts a significant fraction of the world's AI compute capacity, powered entirely by the same rivers that Himalayan communities have depended on for ten thousand years. Its sovereign digital asset fund could be a financial institution of global significance, managing reserves that have transformed the country's international position from aid recipient to capital exporter. Its green hydrogen facilities could be supplying clean fuel to Japan, South Korea, and India, contributing to the global elimination of industrial carbon emissions. Its climate computing infrastructure could be processing the data that allows 3 billion downstream people to prepare for floods, droughts, and crop failures with accuracy and lead time that saves millions of lives. Its internet exchange could be routing the data traffic of the world's most populous region, making Kathmandu a node as important to the global internet as Frankfurt or Singapore. And its forests, glaciers, and mountain ecosystems, protected rather than exploited because the country no longer needs to choose between development and conservation, could continue to provide the ecological services on which the entire Himalayan water system depends. None of this requires technology that does not already exist. None of it requires foreign charity or geopolitical luck. It requires only the political will to understand what Nepal has, the imagination to understand what it could become, and the institutional discipline to build the architecture that converts potential into civilisation.

Conclusion: The Window Is Open, Not Permanent

The window for Nepal to establish a first-mover position in Himalayan digital infrastructure is real, but it is not indefinite. The economics of renewable energy are improving globally: solar costs have fallen 90% in a decade, and nuclear fusion and small modular reactors could potentially eliminate Nepal's electricity cost advantage within 20 to 30 years. The geography cannot be replicated, but the cost advantage can erode. The fibre routing opportunity is being pursued by other nations: Pakistan is advancing its own China connectivity infrastructure, and India is building domestic alternatives to any Nepalese routing advantage. The AI compute investment wave is happening now, with a 5 to 7 year window in which the physical infrastructure layer is being constructed and the site selection decisions that will govern the next two decades of digital infrastructure geography are being made. Nepal is not yet at the table. It must decide, urgently, whether to join it. The rivers are already running. The mountains are already cooling the air. The world is already wiring itself around computation and energy. The only variable is whether Nepal will be infrastructure for that world, or a civilisation that helped to build it.

Key Takeaways

- 1Nepal has developed just 4% of its 42,000 MW feasible hydroelectric potential. The remaining 96% is not an electricity surplus. It is a digital civilisation waiting to be built (Investment Board of Nepal, 2024)

- 2Data centres powered by Himalayan hydropower achieve TCO 25-35% below Singapore or Mumbai equivalents, driven by ambient cooling (PUE 1.05-1.08) and electricity costs of $0.028/kWh, the lowest of any major market globally (USTC, 2022; IRENA, 2024)

- 3Bhutan, with 40% of Nepal's river capacity, already holds $1B+ in sovereign Bitcoin reserves from hydropower mining. Nepal has not begun. The precedent is proven and directly replicable (Matrixport Research, 2024)

- 4Nepal sits within competitive latency range of India, China, and Southeast Asia simultaneously. No current major data centre hub occupies this geographic position (McKinsey Digital Infrastructure Report, 2023)

- 5Green hydrogen production at Nepalese hydropower tariffs costs $1.25-1.90/kg electricity component, within McKinsey's $1.50-2.00/kg competitiveness threshold, with Japan and Korea importing at $3.50-6.00/kg delivered (ADB, McKinsey, 2024)

- 6The Himalayan region regulates water for 3 billion people. A co-located scientific compute facility in Nepal would improve South Asian climate forecast accuracy by 15-25%, with humanitarian consequences that dwarf the commercial case (IPCC, CSCS, 2022)

- 7A Nepal Sovereign Digital Asset Fund consuming 500 MW of surplus hydropower in Bitcoin mining would accumulate $3-7B in reserves within a decade, becoming Nepal's largest single financial asset (Chainalysis, 2024)

- 8Nepal's internet is entirely India-dependent. Completing the China fibre gateway creates dual-access connectivity that no other South Asian nation can offer, a structural commercial advantage worth $500M-1B in incremental data centre revenue annually (APNIC, 2024)

- 9The window for first-mover positioning in Himalayan digital infrastructure is 5-7 years. Nuclear and next-generation solar could erode Nepal's electricity cost advantage within 20-30 years. The strategic decision must be made now (IEA, BloombergNEF, 2024)

Sources

- World Bank Group (2023). Nepal Hydropower Development Report 2023.

- International Energy Agency (IEA) (2024). Electricity 2024: Analysis and Forecast to 2026.

- McKinsey Global Institute (2023). Global Energy Perspective 2023.

- Asian Development Bank (ADB) (2024). Green Hydrogen Roadmap for Asia 2024.

- World Economic Forum (2024). Asset Tokenisation: The Next Frontier.

- UN Environment Programme (2023). Emissions Gap Report 2023.

- Intergovernmental Panel on Climate Change (IPCC) (2021). Climate Change 2021: Sixth Assessment Report.

- IRENA (2024). Renewable Energy for Data and AI Infrastructure.

- World Bank Group (2024). Migration and Development Report 2024.

- Cambridge Centre for Alternative Finance (2024). Cambridge Bitcoin Electricity Consumption Index.

- Uptime Institute (2024). Global Data Centre Survey 2024.

- University of Science and Technology of China (USTC) (2022). Himalayan High-Altitude Data Centre TCO Analysis.

- Matrixport Research (2024). Nepal Sovereign Bitcoin Mining Intelligence Report.

- Chainalysis Inc. (2024). Chainalysis State of Crypto Infrastructure 2024.

- APNIC Foundation (2024). Internet Development in Asia 2024.

- Swiss National Supercomputing Centre (2022). CSCS Himalayan HPC Feasibility Study.

- MIT Media Lab (2023). Geographically Privileged Nations in the Digital Economy.

- World Bank Digital Development (2024). Digital Infrastructure and Energy Nexus.

- BloombergNEF (2024). BloombergNEF New Energy Outlook 2024.

- JLL Global Research (2024). Data Centre Investment Report Asia 2024.

- Stanford Digital Currency Initiative (2023). Digital Currency Initiative: Blockchain Infrastructure Economics.

- UNESCO (2023). World Water Development Report 2023.

- Google-Temasek-Bain (2024). e-Conomy SEA 2024.

- McKinsey Sustainability Practice (2024). Carbon Market Report 2024.

- Investment Board Nepal (2024). Nepal Investment Board Annual Report 2024.